UK Private Pensions

In the UK, there are Defined Contribution pensions (below) and Defined Benefit pensions (click to scroll). Many people call both private pensions.

These pension schemes work very differently. They are funded, managed, taxed and accessed differently. Knowing which pension scheme you are in can help you estimate your future retirement income and understand how much financial risk you carry. Which is better?

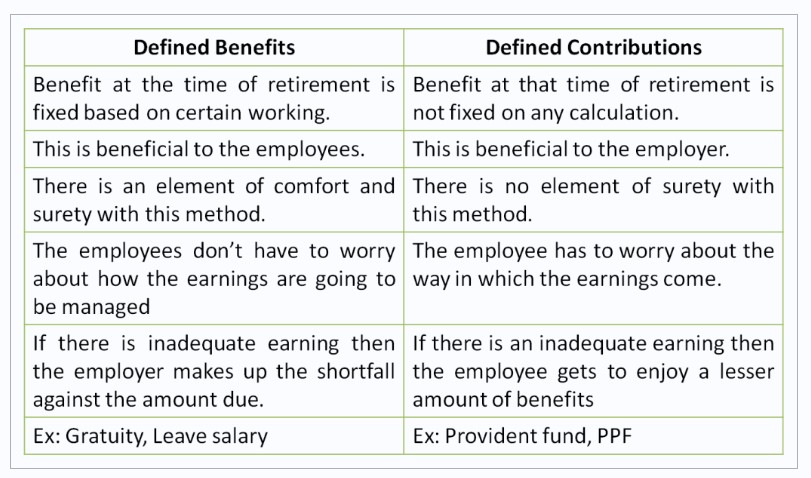

Defined Benefit pensions are often valued for the level of security they provide in retirement. The pension income is usually guaranteed and based on salary and years of service rather than investment performance. In most cases, the employer carries the responsibility for funding the scheme and managing the underlying investments. This means the employee does not normally take on direct investment risk during their working life.

Many Defined Benefit schemes also include inflation protection, which can help preserve spending power throughout retirement. In final salary arrangements, pension benefits are often linked to earnings close to retirement age, which may benefit long-serving employees with higher late-career salaries. Contributions are normally made in a tax-efficient way, allowing retirement savings to grow without immediate income tax on the funds invested. For people seeking predictable long-term income, this type of pension can provide valuable financial stability.

However, Defined Benefit pensions are often more difficult to understand than modern pension arrangements. The rules around accrual rates, retirement ages, survivor benefits, and inflation increases can become complex, particularly across older schemes. They may also be less beneficial for employees who leave an organisation early in their career, as the long-term value is often strongest for those who remain with the employer for many years. In some cases, changing jobs frequently can reduce the overall benefit built up within the scheme.

Defined Contribution pensions offer a different approach and are now the most common type of private pension in the UK. Instead of promising a guaranteed income, they build an investment pot through contributions from the employee, employer, or both. Many people prefer these pensions because they are generally easier to understand and more flexible throughout working life. Contributions are usually made directly through payroll, making regular pension saving straightforward and automatic.

A Defined Contribution pension also allows the individual greater control over how much they contribute and how their pension is invested. If investments perform well over time, the pension pot may grow substantially and provide strong retirement income later in life. These pensions are also portable, meaning they usually stay with the individual when changing employers. This flexibility suits modern careers where people may move between jobs, industries, or countries several times during their working life.

The main disadvantage is that the investment risk sits with the individual rather than the employer. Poor market performance, inflation, or starting pension contributions too late in life can all reduce the value of the final retirement fund. Building a large pension pot may become difficult for those who begin saving later in their career or contribute inconsistently over time. For this reason, regular pension reviews and long-term planning become increasingly important, particularly for people intending to retire overseas.

What Is a Defined Contribution Pension?

A Defined Contribution pension is the most common type of private pension in the UK today.

It is also known as:

- A money purchase pension

- A pension pot

- A workplace defined contribution scheme

- A personal pension

Most modern workplace pensions fall into this category. With a Defined Contribution pension, money is paid into an investment account over time.

Contributions may come from:

- You

- Your employer

- Tax relief from the UK government

The pension provider then invests the money on your behalf.

The final value of your pension depends on:

- How much has been contributed

- How long contributions have been made

- Investment performance over time

- Charges and management fees

- Inflation and market conditions

Unlike some older pension schemes, there is no guaranteed retirement income.

The amount available at retirement depends entirely on the value of your pension investments.

Examples of Defined Contribution Pensions

Examples are:

- Workplace auto-enrolment pensions

- Personal pensions

- Self-Invested Personal Pensions (SIPPs)

- Stakeholder pensions

- Group personal pensions

Many people now build retirement savings through several different Defined Contribution pensions accumulated across multiple jobs.

How Defined Contribution Pensions Work

Each pension contribution purchases investments inside your pension.

These investments are held in:

- Shares

- Bonds

- Property funds

- Index funds

- Mixed asset funds

- Target retirement funds

The value of these investments can rise or fall over time.

For example:

- You contribute £400 per month

- Your employer contributes £300 per month

- Tax relief increases the total contribution further

- The investments grow over 25 years

Over time, the pension pot may become substantially larger than the amount originally paid in.

However, investment growth is never guaranteed.

Economic downturns, inflation, market volatility, and poor investment performance can all reduce pension values.

This means the investment risk largely sits with the pension holder.

When Can You Access a Defined Contribution Pension?

Most Defined Contribution pensions can normally be accessed from age 55.

The minimum pension age is expected to rise to 57 from 2028.

Accessing pension funds earlier is usually only possible in cases involving serious ill health.

Options for Taking Money From a Defined Contribution Pension

One of the main advantages of Defined Contribution pensions is flexibility.

At retirement, there are several ways to access the pension.

Tax-Free Lump Sum

Most people can usually take up to 25% of their pension tax free.

This is commonly known as the Pension Commencement Lump Sum.

The remaining pension funds are generally taxable when withdrawn.

Pension Drawdown

Drawdown allows you to keep the pension invested while taking income gradually.

This has become one of the most common retirement options in the UK.

The pension remains invested after retirement, which means:

- Investments may continue growing

- Income can remain flexible

- The pension may continue benefiting from market growth

- Investment values can still fall

Drawdown provides flexibility but also requires careful planning.

Withdrawing too much too early can significantly reduce retirement income later in life.

Buying an Annuity

An annuity converts pension savings into a guaranteed income.

You exchange part or all of the pension pot for regular payments.

These payments may continue:

- For life

- For a fixed number of years

- Until the death of a surviving spouse or partner

The income available depends on:

- Age

- Interest rates

- Health conditions

- Life expectancy

- Whether inflation protection is included

Taking Cash Withdrawals

Some people take pension money in stages as lump sums.

While this can provide flexibility, large withdrawals may trigger significant income tax liabilities if not managed carefully.

How to Tell If You Have a Defined Contribution Pension

You probably have a Defined Contribution pension if your pension statement shows:

- A pension pot value

- Investment balances

- Fund performance

- Contribution totals

- Projected retirement values

Typical wording:

- Current pension value

- Estimated future fund value

- Contributions paid this year

- Investment growth

The focus is usually on the value of investments rather than guaranteed retirement income.

Risks of Defined Contribution Pensions

Defined Contribution pensions offer flexibility and investment potential, but they also involve risks.

Common risks:

- Investment losses

- Inflation reducing spending power

- Poor market performance near retirement

- Running out of money later in life

- High pension fees

- Poor withdrawal planning

- Currency risk for overseas retirees

Managing these risks often requires regular reviews and careful retirement planning.

What Is a Defined Benefit Pension?

A Defined Benefit pension provides a guaranteed retirement income.

It is often called:

- A final salary pension

- A career average pension

- A salary-related pension

These pension schemes were historically common in:

- The public sector

- Government employment

- Large corporations

- Older private sector firms

Many Defined Benefit schemes are now closed to new members because they are expensive for employers to maintain.

How Defined Benefit Pensions Work

Instead of building an investment pot, Defined Benefit pensions promise a set level of income in retirement.

The amount paid is usually based on:

- Salary

- Years worked for the employer

- A scheme accrual rate

For example:

- A pension scheme offers 1/60th accrual

- You work there for 30 years

- Your pensionable salary is £60,000

Your annual pension may be:

30/60 × £60,000 = £30,000 per year

Unlike Defined Contribution pensions, the investment performance of the pension fund does not directly determine your retirement income.

Final Salary vs Career Average Pensions

Final Salary Pension

A final salary pension uses earnings near retirement to calculate pension income.

This means promotions or salary increases late in your career can significantly improve pension benefits.

Career Average Pension

A career average pension calculates pension income based on average earnings across your working life.

This type of scheme is now more common in modern public sector pensions.

Benefits of Defined Benefit Pensions

Defined Benefit pensions are often considered valuable because they may provide:

- Guaranteed income for life

- Inflation-linked increases

- Spouse or dependent benefits

- Greater income predictability

- Lower personal investment risk

In many cases, the employer carries the financial and investment risk rather than the employee.

How to Tell If You Have a Defined Benefit Pension

You probably have a Defined Benefit pension if your pension statement shows:

- Estimated yearly retirement income

- Years of pensionable service

- Accrual rates

- Pensionable salary

Typical wording:

- Current pension earned per year

- Estimated retirement income

- Pensionable service

- Normal retirement age

The statement usually focuses on annual retirement income rather than investment balances.

Important Considerations for Defined Benefit Pensions

Reducing Hours Before Retirement

If you are in a final salary scheme, reducing your hours before retirement could reduce your pension income.

Some schemes use your salary close to retirement when calculating benefits.

A lower salary shortly before retirement may permanently reduce the pension paid for the rest of your life.

Before moving to part-time work or accepting a lower-paid role, it is important to check the pension scheme rules carefully.

Pension Transfers

Some people consider transferring Defined Benefit pensions into Defined Contribution pensions.

This is a major financial decision.

A transfer may provide:

- Greater flexibility

- Access to larger lump sums

- Inheritance planning opportunities

However, it also means giving up guaranteed income.

In many cases, regulated financial advice is legally required before a Defined Benefit transfer can proceed.

How Pension Tax Rules Differ for Expats

For British expats, pension tax planning can become far more complicated once living overseas.

The country you live in may have completely different tax rules from the UK.

The amount of tax you pay can depend on:

- Your country of residence

- Your tax residency status

- The type of pension you receive

- Double taxation agreements

- Whether pension income is transferred overseas

- How pension withdrawals are structured

Many expats wrongly assume that UK pension tax rules automatically apply abroad.

This is not always correct.

A pension withdrawal that receives favourable treatment in the UK may be taxed differently once you become tax resident overseas.

UK Tax Residency and Pension Income

Your UK tax residency position remains important even after leaving Britain.

If you remain UK tax resident, pension income is normally taxed in the UK under standard income tax rules.

However, once you become non-resident for UK tax purposes, the position may change significantly.

Many countries have double taxation agreements with the UK. These agreements are designed to prevent the same pension income being taxed twice.

Depending on the treaty involved, pension income may become taxable:

- Only in the UK

- Only in your country of residence

- In both countries, with tax relief available

The exact treatment depends on both the country involved and the type of pension being received.

For example, private pensions, government pensions, and State Pension income may all receive different tax treatment.

Example: British Expats Living in Thailand

Thailand remains one of the most popular retirement destinations for British expats in Asia.

A British retiree living in Thailand may receive:

- UK State Pension income

- Workplace pension income

- SIPP withdrawals

- Pension drawdown income

- Rental income from the UK

Once considered tax resident in Thailand, pension income transferred into Thailand may potentially become taxable under Thai tax rules.

For example:

- A retiree withdraws £25,000 from a UK pension

- The money is transferred into a Thai bank account

- Thai tax residency rules may apply to those transferred funds

This can create confusion because pension withdrawals treated favourably in the UK may not receive identical treatment overseas.

For example, many people assume that the 25% tax-free lump sum available in the UK automatically remains tax free abroad.

That is not always the case.

The local tax rules of the country where you live may still apply.

Thailand-based retirees may also face currency risk.

If sterling weakens against the Thai baht:

- Rent may become more expensive in pound terms

- Healthcare costs may rise

- Everyday spending power may fall

- Retirement budgets may become less predictable

This is one reason why many overseas retirees monitor exchange rates closely.

Example: British Expats Living in Spain

Spain taxes residents on worldwide income.

A British expat living permanently in Spain may therefore become liable for Spanish tax on UK pension income.

This can include:

- Defined Contribution pension withdrawals

- Pension drawdown income

- Workplace pension payments

- State Pension income

Large pension withdrawals can sometimes push retirees into higher tax bands.

For example:

- A retiree takes a large lump sum to buy property

- The withdrawal increases annual taxable income significantly

- Higher tax rates may then apply

Government service pensions may sometimes follow different treaty rules.

Certain public sector pensions may continue being taxed in the UK even while the pension holder lives abroad.

Example: British Expats Living in Portugal

Portugal has long been popular with British retirees because of its climate, healthcare system, and lifestyle.

Tax rules in Portugal have changed several times in recent years.

This highlights an important issue for expats.

Tax planning overseas is rarely static.

A pension structure that appears tax efficient today may not remain efficient indefinitely.

A retiree living in Portugal may need to consider:

- Local income tax rates

- Residency rules

- Changes in pension taxation

- Currency exposure

- Estate planning rules

Regular reviews become increasingly important as tax laws evolve.

Currency Risk for Overseas Retirees

Many British expats receive pension income in pounds while spending money in another currency. This creates exchange rate exposure. If the pound weakens against local currencies, overseas living costs may effectively increase.

For example:

- £2,000 per month may previously convert comfortably into baht or USD but,

- A weaker exchange rate may reduce the same pension income substantially

- Day-to-day living costs may rise without pension income increasing

This can affect:

- Housing costs

- Medical expenses

- Insurance premiums

- Travel budgets

- Long-term retirement planning

Overseas Pension Transfers

Some expats consider transferring UK pensions overseas.

Potential reasons?

- Simplifying retirement administration

- Reducing ongoing currency conversions

- Accessing different investment options

- Aligning retirement planning with country of residence

However, overseas pension transfers can also create significant risks. These may be:

- Tax complications

- Transfer charges

- Loss of UK protections

- Investment risk

- Currency volatility

- Regulatory differences

Transferring pension funds internationally should never be treated as a routine administrative decision. The long-term consequences can be substantial.

Understanding both UK pension rules and the local tax rules where you live is essential before making major retirement decisions overseas.