If you live outside Britain, the UK can still tax your UK source income, such as when selling a property. This also includes rental income, some pensions, and work physically done in the UK. If you’re confused about UK tax for non-residents, read on or contact us for professional help.

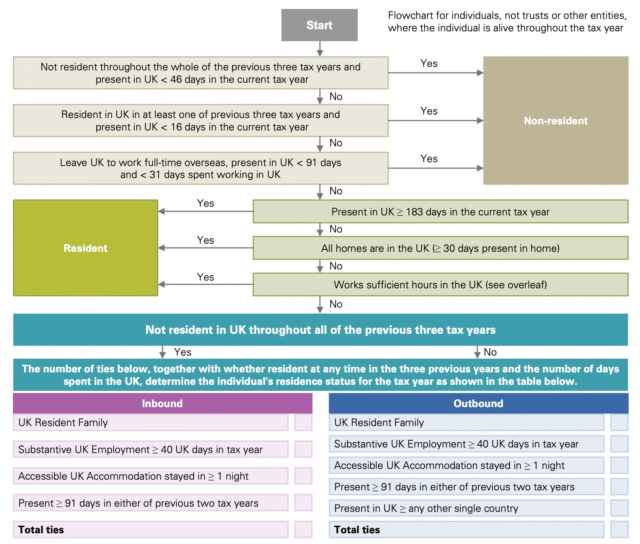

The Statutory Residence Test (SRT) decides which camp you are in, not your postcode or what your mate at the pub reckons.

Keep day counts + evidence like flights and leases which will help your case and save you money.

Adam’s tip to prepare for residency tests

Who is commonly affected by UK tax for non-residents

- UK landlords living overseas, especially long-term expats with one or two rentals.

- Anyone doing short stints of work in the UK while living abroad.

- People retiring offshore with a mix of State Pension, private pensions and UK savings.

- Leavers and returners in a split year where income timing matters.

What to do

- Confirm residence with the SRT. If you are non resident, the UK still taxes UK source income. If you leave or arrive part way through the year, you may claim Split Year on SA109. GOV.UK

- Landlords, apply to the Non Resident Landlord scheme so rent is paid gross, then file Self Assessment to settle the real tax. If you do not, letting agents or tenants withhold 20 percent by default. GOV.UK

- Selling UK property while non resident, report and pay any UK CGT within 60 days of completion. GOV.UK

Mini case study

Jim moved to Thailand, left his flat on a managed let, and assumed he would deal with tax later. The agent withheld 20 percent for months, strangling his cash flow. He applied for NRL approval, switched to gross rent, then filed SA to claim repairs and mortgage interest relief correctly. Net cash recovered, stress lowered.

Common traps

- Assuming non residence equals no UK tax, as UK source income can still be taxable.

- Missing the 60 day property reporting deadline.

- Forgetting SA109 when claiming non residence or split years.

If you are unsure, we will connect you to qualified advisors to review your position, set up the right filings, and bolt on a quick State Pension check while we are at it.

Sources and further reading

- HMRC – Tax if you live abroad and have UK income: https://www.gov.uk/tax-uk-income-live-abroad/print

- HMRC – Apply as an individual to receive UK rental income without UK tax deducted (NRL1): https://www.gov.uk/guidance/apply-as-an-individual-to-receive-uk-rental-income-without-uk-tax-deducted

- HMRC – Tell HMRC about Capital Gains Tax on UK property or land if you are not a UK resident: https://www.gov.uk/guidance/capital-gains-tax-for-non-residents-uk-residential-property

- MoneySavingExpert forum, Non-Resident Landlord Scheme experiences: https://forums.moneysavingexpert.com/discussion/5926539/non-resident-landlord-scheme and https://forums.moneysavingexpert.com/discussion/5123234/rental-income-tax-for-non-resident-landlords

Government jargon to understand

Days Spent

An individual spends a day in the UK for SRT purposes if he is in the UK at the end of the day.

However, he is not treated as spending a day in the UK if the day is considered a transit day with no work or the individual is in

the UK due to specified exceptional circumstances beyond his control for a maximum of 60 days. In certain circumstances an

individual will be deemed to spend a day in the UK even though he is not in the UK at the end of the day.

Working full-time overseas (WFTO)

The individual must work sufficient hours overseas (average of 35 hours per week disregarding certain defined days) in the tax

year with no significant breaks from overseas work and spend fewer than 91 days in the UK and work (in this instance for more

than three hours a day) in the UK for fewer than 31 days.

All Homes are in the UK

An individual will be regarded as resident if the individual has a home in the UK for more than 90 days in which the individual is

present on at least 30 separate days in the relevant tax year. In addition for 91 consecutive days, at least 30 of which are in the

tax year, the individual must have no home overseas in which the individual is present on 30 separate days in the tax year. If the

individual has more than one home in the UK, the test must be met in relation to at least one of those homes when considered

separately from the other home(s).

Works Sufficient Hours in the UK (WSHUK)

The individual must work sufficient hours in the UK over a 365 day period (average of 35 hours per week disregarding certain

defined days where all or part of the 365 day period is in the current tax year) with no significant breaks from UK work. More

than 75% of the days in the period when the individual does more than three hours work per day must be worked in the UK and

the individual must work for more than three hours in the UK on at least one day in the current tax year.

Workdays

A work day in the UK for the purposes of the SRT is a day on which more than three hours work is performed. Work includes

incidental and non incidental duties and most travel. There is a complicated test to determine whether an individual works

sufficient hours in the UK or overseas for the WFTO or the WSHUK tests.

Although the distinction between incidental and substantive duties is not relevant for the purposes of the SRT the distinction

remains important for the purposes of calculating the tax liability of employees. When the employee is regarded as being non

UK resident, incidental duties will continue to be deemed to be performed offshore and only substantive UK duties are taxable.

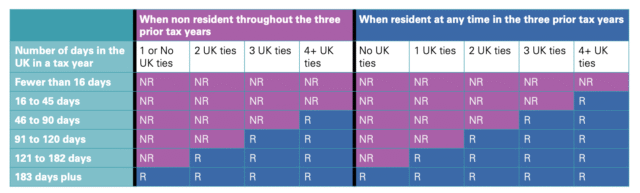

Sufficient Ties Test

When an individual does not meet any of the automatic overseas tests nor any of the automatic UK tests, the individual’s

residence will depend upon the number of UK ties (or connections) the individual has and the number of days spent in the UK.

UK resident family

A family tie exists if a person’s spouse, civil partner or minor child is resident in the UK in the relevant tax year. A person with

whom the individual is living as husband and wife or as if they were civil partners is also included. Where a minor child is UK

resident because they are in full-time education in the UK, they will not be treated as UK resident for family tie purposes unless

they spend more than 20 days in the UK outside of term time during the tax year.

Split years

Although an individual can only be regarded as resident for a complete tax year, special rules apply when an individual

commences or ceases residence which are outside the scope of this flowchart. The tax year may be spilt in to an overseas part

and a UK part for certain purposes.